Inland’s Keith Lampi and Mountain Dell’s Taylor Garrett Discuss the Current 1031 Exchange Market

Keith Lampi, president, director and chief operating officer of Inland Private Capital Corporation, and Taylor Garrett, managing director of Mountain Dell Consulting, discuss the state of the 1031 exchange market during the first half of 2020.

Keith Lampi, president, director and chief operating officer of Inland Private Capital Corporation, and Taylor Garrett, managing director of Mountain Dell Consulting, discuss the state of the 1031 exchange market during the first half of 2020.

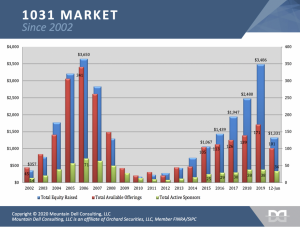

How much equity was raised in the securitized 1031 market in Q1 and Q2 of 2020? How does the first half of the year compare to 2019?

Taylor Garrett: According to the numbers provided to us:

2020: Q1: $1.05 billion, Q2: $410 million.

2019: Q1: $670 million, Q2: $692 million

What is your projection for aggregate industry sales for all of 2020?

Taylor Garrett: I am a bit more bullish than I was 60 days ago. I believe we will get to $2.0 – 2.5 billion in equity by year end.

Given the dislocation in the marketplace, are you seeing any trends emerge in terms of sponsor activity, in the way of new market entrants or consolidation in market share among existing market participants?

Garrett: We haven’t seen a lot of consolidation yet. We have heard of new sponsors looking to enter the space, but we are at 34 sponsors that have had live offerings this year. This is comparable to last year. I think later this year and early next year is where we would see consolidation. Right now, it seems too early for that to happen.

As the industry’s top securitized 1031 sponsor, how does IPC perceive the rest of 2020 from a market demand perspective, and how are you approaching bringing new products to market?

Keith Lampi: We experienced a cooling effect in market demand throughout April and into May. Market volatility and general uncertainty led many buyers and sellers to hit the pause button on pending transactions.

For 1031 investors, who under normal circumstances have a time-imposed compulsion to transact, the “wait and see” impact on transaction volume was intensified by the IRS imposed extension on 45/180 day deadlines through July 15th.

As the industry has settled into a “new norm” it is clear that transaction volume will continue to remain down from peak market levels for the foreseeable future. However, unlike the recession of 2008/9, when transaction volume came to a halt mainly due to the lack of availability of financing, the market today is quite different.

Financing in many sectors is readily available and at a historically low cost of capital, which has created a healthy environment for buyers and sellers to continue to come together. I believe this trendline which has begun to show an uptick in market demand, should continue to accelerate into the second half of the year.

In terms of new products, we are taking a measured approach with asset selection by sector and market and long-term investment performance in mind. Maintaining a high quality, diverse inventory base to accommodate 1031 investor demand is a core objective of IPC.

The sectors and markets that appear best positioned for long term stability are not necessarily trading at discounts to pre-pandemic levels. This means, once post pandemic underwriting standards are incorporated, new products will likely experience yield compression, at least near term.

What are the differences you are seeing between the period of dislocation that occurred in 2008/2009 during the financial crisis, compared to today from a commercial real estate perspective?

Taylor Garrett: So far this seems very different. The biggest challenge in 2008 had a lot more to do with a credit crisis. Keep in mind, as well, that with the prior downturn, most of the market was focused on TICs. This time, it’s DSTs, which are, of course, different.

A big challenge in 2008 was most TIC products were multi-tenant office and multi-tenant retail. That is no longer the case in today’s DST environment.

A big concern for the industry this time around was “collections” for multifamily and all asset types. So far, the collections for multi-family have stayed relatively strong. There are pockets where some programs have been more hard-hit markets but, generally speaking, it has not yet been a huge problem for multifamily.

What do the capital markets look like today in terms of availability of debt, pricing and how do the capital markets compare to late 2019 and early 2020?

Keith Lampi: After the onset of the pandemic, the federal reserve implemented numerous programs that have been well publicized to create stability in the market in relatively short order. Looking at where the capital markets stand today, particularly with respect to real estate financing, there are several positive trend lines throughout marketplace, however variation does exist depending on the asset class and lending source.

More than 50 percent of the securitized 1031 market has been comprised of apartments for the past several years. Agency financing (Fannie-Freddie) remains readily available, however the implementation of index-floors and additional reserve requirements to protect against market uncertainty are the new normal. The rates on 10-year financing are in some instances up to 50 bps lower than pre-pandemic levels. While a majority of 10-year loans at the end of 2019 and early 2020 had interest rates as low as 3 percent, now debt quotes are around 2 percent on similar assets today.

Life insurance companies have also shown notable movement back into the market, albeit with more selectivity on assets and a desire to keep leverage at moderate levels. Banks vary widely: some are staying active with strong sponsor/relationship clients; while others are taking a more wait-and-see approach as they review their portfolio performance.

Conduit and debt funds were greatly impacted by market volatility and benefited the least from the government intervention; some new loan activity has occurred recently, but it will likely be a slow, incremental comeback for this financing source.

Next to multifamily, industrial/warehouse is the most financeable asset type in this market. Office depends on the asset and market. Then as expected, shopping centers and hospitality are very challenging to finance at this time, and most owners and lenders are still in the midst of deferral conversations.

Specialty assets classes have a mixed view largely dependent on market and strategy, but generally have less suitors. The outlier in the specialty asset class segment is self-storage, which continues to be viewed as the strongest of specialty asset types in today’s environment.

Which asset classes have been targeted and deemed as most desirable by investors in the post-COVID 19 era?

Taylor Garrett: In terms of equity raised, the three asset types that seem to continue to have success are multi-family, net lease, and self-storage. Under multi-family we have seen success on traditional apartments and 55+ active adult living apartments. We have seen much less success with student housing with the complications with universities deciding to go back or not in the Fall. Where that settles out remains to be seen.

Have you begun to see an uptick in investor appetite as we near the July 15th deadline imposed through the IRS extension?

Keith Lampi: Towards the second half of June we began to see a significant uptick in investor demand which has occurred in various forms.

The first subset of investors simply decided to move forward with their investments after several months of tracking operational performance on the various DSTs they had previously identified.

Another category of increased demand has occurred, where investors had previously planned to use DSTs as a “plan B” to their preferred real estate investment property. As a result of the pandemic, many of these investors ran into difficulty completing the purchase of their “plan A” asset and pivoted to moving forward with various DST offerings that were also identified.

Finally, we have observed instances where investors had waited until the first couple of weeks of July to consider and compare paying taxes and cashing out vs. completing an exchange. After tracking market performance, many investors obtained a level of comfort with the underlying assets, sector and market as a whole and decided to complete their exchange.

While all the reasons are different in nature, the common theme is that investors seem to be cautiously optimistic in moving forward with their investments in today’s environment.

Which real estate sectors does IPC believe are best equipped to handle this economically challenging time?

Keith Lampi: Given the diverse footprint of Inland Private Capital’s assets under management, I believe we have a unique perspective from a sector, market and performance standpoint. When I consider the sectors that are well positioned on a forward-looking basis, my analysis begins with considering which sectors have experienced general stability over the course of the past 16 weeks.

The list of best performers in recent weeks is well documented: multifamily, self-storage, healthcare, credit tenant NNN retail, and office. Since most real estate investing strategies in the securitized 1031 market are typically anchored on a long-term analysis, it is not enough to only consider the recent past, we also have to consider how each asset will perform over the long run.

From IPC’s perspective, strategies that are driven by demographic trends and less reliant on economic growth are the areas we plan to focus on near term. These strategies include multifamily, self-storage and healthcare-related assets.

How has asset performance fared throughout the past 12 weeks of the pandemic and how is the industry better equipped to handle this period of uncertainty compared to periods of volatility in the past?

Taylor Garrett: On one hand, there is a general aspect to it, as COVID has certainly impacted the world in which we live. But how it impacts specific asset classes in specific locations has much more variability.

That said, even though we are still earlier in this pandemic than any of us would like to be, I think the DST marketplace is well-positioned to have institutional quality real estate that is pre-packaged for 1031 investors.

We are hearing more and more that investors like the opportunity to invest into higher quality real estate than they could buy on their own, and that they have professional asset and property management to help navigate this unique time. I believe that, long term, we will continue to see the DST marketplace grow because of the opportunity for investors to diversify for as little as $100,000 and have pre-packaged real estate with loans in place and strong operating partners.

It is difficult to know what the future holds, or what the “new normal” will be, but as long as we stay focus on fundamentals and the things that matter most, I really like the prospects that our industry has as we go forward.

Click here to visit The DI Wire directory sponsor page.